Veli Partners with BitDegree to Empower Financial Advisors Through Crypto...

Veli Partners with BitDegree to Empower Financial Advisors Through Crypto...

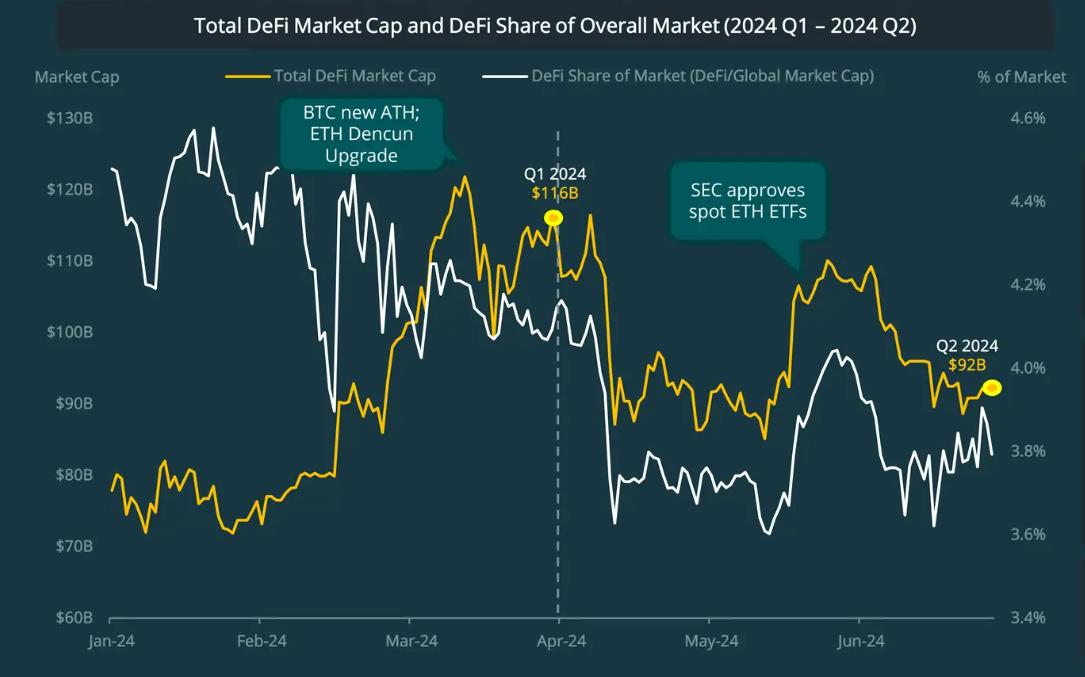

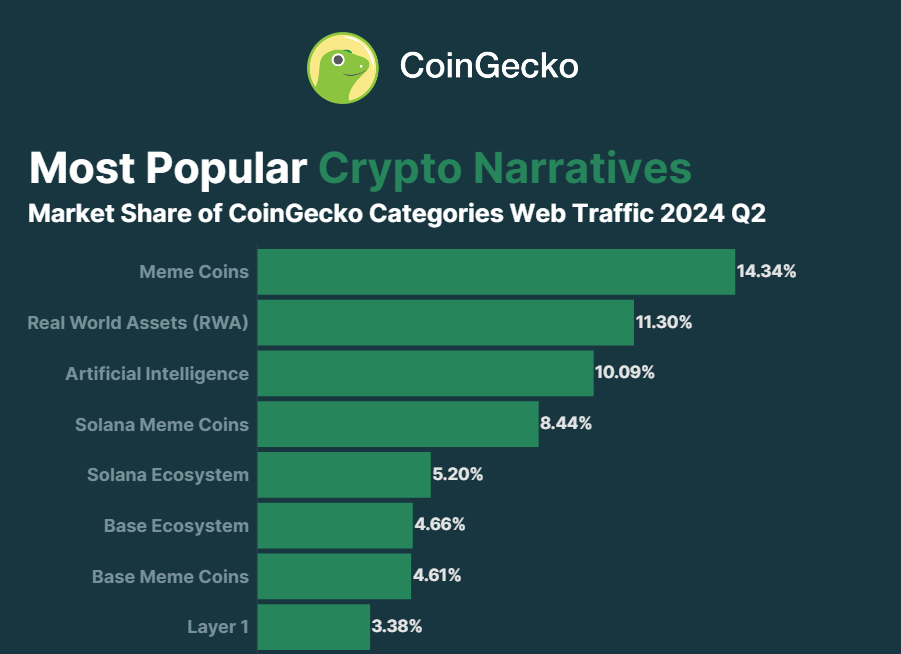

Q1 2025 Market Report This report will cover all the...

Veli is Going for the MiCA License! A new era...